Startup = Growth (YC)

Popular Essay (written September 2012) by Paul Graham from Y Combinator: Startup = Growth

A startup is a company designed to grow fast. Being newly founded does not in itself make a company a startup. Nor is it necessary for a startup to work on technology, or take venture funding, or have some sort of "exit." The only essential thing is growth. Everything else we associate with startups follows from growth." - Paul Graham

Essay summary (2015)

source http://www.startupdiscuss.com/2015/08/paul-graham-startup-growth.html

Redwoods

The central idea of this section is that it is not enough just to serve customers -- that is what a business is after all -- but it must also scale, and to scale by design from their inception. Many startups or software companies because software scales so easily. The challenge for these companies to find something that delights users.

Ideas

First, Graham points out that because the startups are after such huge markets, and the rewards are so high, the solution space has been well explored, and there is a lot of competition.

However, in some areas, technology moves so fast that it produces new opportunities ("Rapid change in one area uncovers big, soluble problems in other areas"), and new solutions to problems, ("startups create new ways of doing things, and new ways of doing things are, in the broader sense of the word, new technology.")

Contrast It would be instructive to compare this to Peter Thiel's advice on ideas, which is to ask yourself what facts you know to be true, but with which most people disagree. Graham's advice seems to be forward looking having to do with new technologies, and new opportunities. Thiel's advice seems to be more introspective because you aren't told to look for an unpopular truth. Q: Do readers think they disagree with each other, agree with each other, or have different opinions that are fundamentally compatible?

Rate

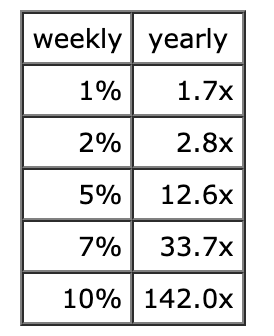

This section is about the growth rate, which is what the whole essay is really about. Graham makes the point that the growth is S shaped and the middle high growth area is what startups aspire to achieve. The best part though is concrete numbers and what they measure:

A good growth rate during YC is 5-7% a week. If you can hit 10% a week you're doing exceptionally well. If you can only manage 1%, it's a sign you haven't yet figured out what you're doing.

The best thing to measure the growth rate of is revenue. The next best, for startups that aren't charging initially, is active users. That's a reasonable proxy for revenue growth because whenever the startup does start trying to make money, their revenues will probably be a constant multiple of active users. (Paul Graham)

When Graham talks about the finding the growth part of the S curve, he sounds closest to Marc Andreessen talking about product market fit.

Q: I would think that the value of a growth rate would depend on the stage of the company. However, he is correct in that any example where I tried 1% per week, I didn't come up with a viable company when the starting point is, say, 10,000 users.

Compass

Graham asserts that the centrality of growth as the metric for success allows founders to focus, and quickly decide between competing claims on their time and attention. He also finds it to be a good way to come up with new ideas en route to solving problems.

Value

Growth rates compound so our intuitions are usually wrong about how fast things can grow and how large they can become:

Deals

Graham describes the motivations for the various actors in a startup story.

Investors get a good risk to return ratio with the added benefit of closely aligned goals because, he claims, capital gains are harder to game than dividends because it is down the waterfall after expenses, salaries etc are paid out.

Founders get to more control of their startup by accepting venture funding.

Finally, acquirers get access to growth.

Understand

Graham summarizes his own argument so well, I'll just quote him again:

If you want to understand startups, understand growth. Growth drives everything in this world. Growth is why startups usually work on technology—because ideas for fast growing companies are so rare that the best way to find new ones is to discover those recently made viable by change, and technology is the best source of rapid change. Growth is why it's a rational choice economically for so many founders to try starting a startup: growth makes the successful companies so valuable that the expected value is high even though the risk is too. Growth is why VCs want to invest in startups: not just because the returns are high but also because generating returns from capital gains is easier to manage than generating returns from dividends. Growth explains why the most successful startups take VC money even if they don't need to: it lets them choose their growth rate. And growth explains why successful startups almost invariably get acquisition offers. To acquirers a fast-growing company is not merely valuable but dangerous too. (Paul Graham)